AI for Social DeFi: Empowering Peer-to-Peer Lending and Crowdfunding

Building on discussions of decentralized IDs, credit scoring, and insurance, this post moves to the future of peer-to-peer lending and crowdfunding. Earlier entries explored the shortcomings of legacy credit scoring systems and demonstrated how blockchain technology and AI protocols can create more equitable and secure alternatives. Similarly, our exploration of AI-driven improvements in insurance through automated parametric execution exposed the inefficiencies and outdated nature of traditional insurance infrastructure. This article applies a similar lens to legacy peer-to-peer lending and crowdfunding services.

We begin by expanding on the foundation laid in our credit scoring article, outlining the key distinctions between traditional and decentralized lending models. Next, we examine how blockchain technology, through DeFi protocols, can unlock funding opportunities and broaden access for those historically excluded from financial systems. We then turn to crowdfunding, exploring how integrating blockchain and AI can enhance these services. e’ll conclude with a look at the potential future of these evolving markets.

Traditional vs DeFi Lending Protocols

When Bitcoin was first launched in 2009, it paved the way for global decentralized currencies. One of the more overlooked secondary effects of this technology has been the underlying basic banking infrastructure required to execute it. It allowed anyone with an internet connection to store and transact value with another party without needing to go through expensive and inefficient third-party intermediaries.

Blockchain technology enabled a free bank account for anyone with an internet connection. This offered an essential lifeline to the estimated 1.4 billion unbanked people worldwide. With the introduction of smart contracts, more advanced banking instruments became available, including peer-to-peer lending protocols like Aave.

The launch of Bitcoin in 2009 introduced the world to decentralized currencies, but its impact went beyond a new form of money. It also established an alternative banking infrastructure. Practially, Bitcoin provides a free and accessible form of banking to anyone online.

Credit Risk Analysis

As we saw in our post about decentralized credit scoring, the legacy risk analysis metrics used in loans are skewed toward larger, more trusted borrowers. This makes accessing credit more difficult and expensive, limiting its availability to those who need it most and making microloans overly cost-prohibitive to execute on a large scale. Fortunately, the convergence of blockchain technology and AI can offer novel solutions.

Peer-to-peer lending protocols shift the risk dynamic from the borrower to the lender. While this has always technically been the case with legacy institutions, their use of outdated risk assessment software often generates unfavorable terms for low creditworthiness borrowers. Blockchain technology and AI can create more dynamic risk assessment models that incorporate social patterns, transaction histories, and on-chain behaviors to better determine the likelihood that a person will be able to repay loans. This ultimately lowers the interest on loan payments, creates an automated creditworthiness report, and opens the doors for microloans as a pathway to accessing larger loans without trapping borrowers under oppressive payment plans.

The use of dynamic peer-to-peer lending models combined with decentralized autonomous organizations (DAOs) allows for more advanced cooperative movements. Members can more easily participate in decision-making votes on how and where to distribute funds, allowing the over a billion unbanked people globally to participate in the governance themselves and determine where to distribute microloans.

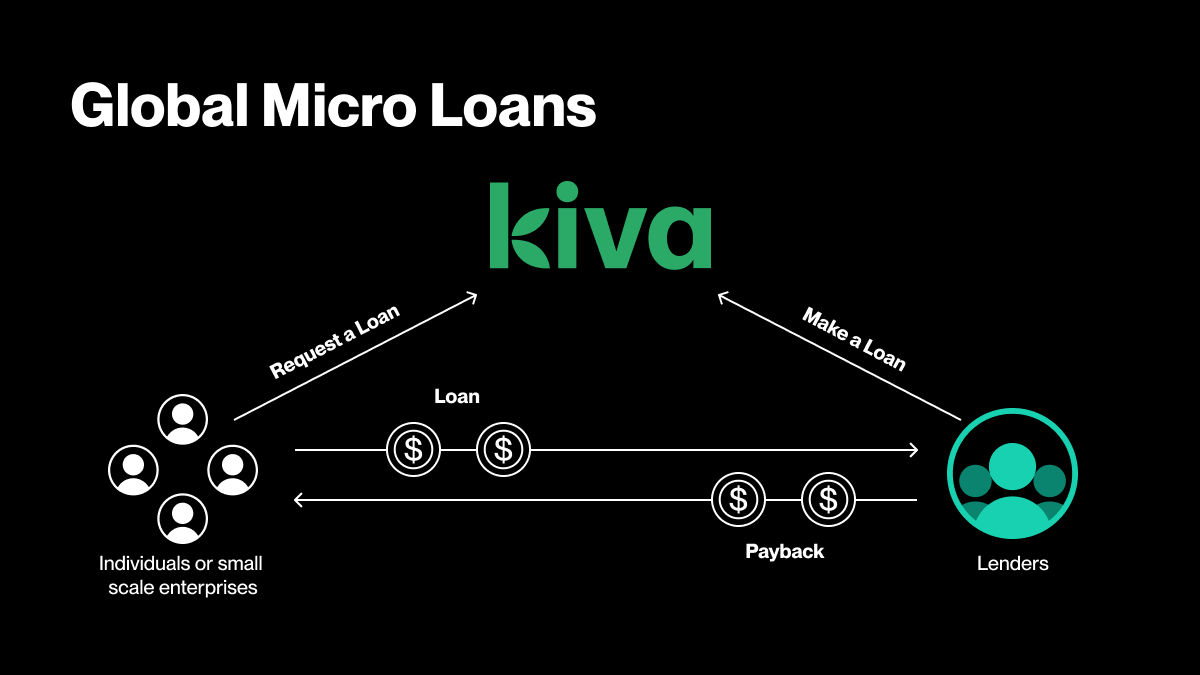

Global Microloans

Kiva.org has been active as a microloan leader since 2005 and specializes in providing low-interest microloans for underserved communities around the world. Some of the site’s most utilized loan applications are from refugees, women, and people living in regions most impacted by climate change. The company has raised over $176 million in over sixty-two countries with donations starting at $25.

Despite Kiva's success, it remains a centralized provider and therefore still prone to certain inefficiencies that blockchain technology and AI protocols could improve. Blockchain technology eliminates the need for international wire transfers, which can be costly and administratively cumbersome. For smaller loans, wire transfers are simply too onerous. Blockchain technology can facilitate direct peer-to-peer funding and remove the minimum donation requirement of $25 from lenders. This opens the doors for even smaller and more dynamic payment options that could be spread out over time for a borrower.

The Next Generation of Crowdfunding

The popularity of digital crowdfunding software like GoFundMe has provided unparalleled access to coordinated charitable donations. GoFundMe has raised over $30 billion from over 150 million people since launching in 2010. Yet, despite the immense contributions that crowdsourcing projects have made, there are still areas for improvement. Similar to the example of Kiva, international crowdfunding still must overcome the inefficiencies of legacy banking infrastructure when it comes to dispersing funds across borders. Blockchain technology opens up near instant final settlement with the option for more dynamic distribution methods.

Instant Global Charity Funding

In all the mania that memecoins brought throughout 2024, a few projects tapped into the charitable nature of the global crypto community. Most notable was the case of Runway Finance’s co-founder Siqi Chen’s daughter’s memecoin namesake $MIRA. In December 2024, Chen posted his GoFundMe campaign seeking funding for his daughter’s rare Adamantinomatous Craniopharyngioma brain cancer research. The Pump.fun and broader Solana community saw the opportunity to leverage their popular ecosystem and created a memecoin to match the GoFundMe campaign.

The memecoin went viral and shot up to over $80 million valuation, of which Chen was given 50% of the supply. He committed to selling off his supply and donating the profits to the Hankinson Lab at the University of Colorado. He transparently sold off $1000 worth of $MIRA every 10 minutes. The original GoFundMe account was set up to deliver $300,000 for research. Within a few days, Chen had successfully sold off over $1 million worth of $MIRA, demonstrating the raw potential of decentralized crowdfunding.

Zero-risk Lottery Services

In addition to the charitable and cooperative nature of crowdfunding, blockchain technology unlocks some unique opportunities for investors. Zero-loss lottery services may appear to be nothing more than a scam, and under legacy financial infrastructure, that is likely. However, specialized consensus mechanisms like proof of stake (PoS) and peer-to-peer lending protocols open up opportunities that reward users for staking their assets without risking the assets themselves.

PoolTogether is one blockchain project that leverages a social financing apparatus and applies blockchain technology to create new opportunities. The process works by creating a pool where users deposit $USDC. The pool of funds is then routed to a lending protocol like Aave, where the funds are lent out. The funds earn interest accrued every ~15 seconds, which is returned to the pool. The pool then leverages the Chainlink Verifiably Random Function (VRF) protocol to select a winner and reward the user with the funds.

Users can withdraw their funds anytime, allowing for a riskless lottery service. Since the lottery prizes are generated from lending and staking mechanics, none of the users' initial deposits are lost. AI could be leveraged to further enhance the operation of PoolTogether and other similar riskless lottery services by introducing secure cross-chain equity pools and limiting exposure of loan defaults through advanced anomaly risk detection protocols.

The Future of Peer-to-Peer Lending and Crowdfunding

AI can improve the peer-to-peer lending process by introducing advanced anomaly detection protocols to quickly identify bad actors within a system. More loans can be evaluated and issued by having immutable repayment plans combined with automated AI risk assessment protocols. The same process can leverage more advanced creditworthiness assessments, considering social patterns, transaction histories, and on-chain behaviors. This all provides opportunities to users and regions typically underrepresented in legacy credit rating systems.

We have also seen how blockchain technology’s unique architecture can open the door to more novel crowdfunding practices like zero-loss lottery pooling and hypergrowth memecoin donations. AI chatbots have underpinned the rise in memecoin launch platforms like Pump.fun and opened the door to new levels of charitable fundraising.

Peer-to-peer lending and crowdfunding legacy markets have offered lifelines for millions of people. Blockchain technology and AI protocols allow these markets to evolve into a more dynamic space that can offer immediate relief for charities and borrowers. They also enable more diverse and equitable lending practices for regions historically locked out of international finance. As global macroeconomic events become more unstable due to climate change, regional tensions, and combative global trade relations, decentralized peer-to-peer lending and crowdfunding options powered by AI can give everyone added resiliency.